This article is an on-site version of the Unhedged newsletter.sign up here Send newsletter directly to your inbox on weekdays

Summer is over. What a drug. S & P-Despite its small but perceptible undercurrent fear -Increased 8% between Memorial Day and Labor Day. That’s all for “sell away in May”. Fall may include tapering asset purchases, slowing profit growth and economic fundamentals. But what does it rhyme to “sell in September”?

Retail flow (Part 1)

There was something interesting piece In yesterday’s FT, based on JP Morgan’s research notes, we talked about how the surge from individual investors to individual equities and ETFs is supporting the stock market. The key chart of the work is as follows.

This is a very impressive chart, but I have to confess that I don’t know how JP Morgan came up with these numbers. The report itself states: [the chart] The above method captures only price-improved market orders, which make up about 45% of total retail volume, so the actual netflow is at least twice as underreported. This doesn’t make things very clear to me, oh. Let’s look at the details, but for now, let’s assume the data is in the right direction.

Here are some important quotes from the FT work:

Nikolao Spanigilzoglow, a cross-asset research analyst at JP Morgan, said: “If that trend stops, especially when we see significant outflows from equity ETFs, we need to start worrying about the stock market.”

In addition, let me confess that I don’t know how to evaluate the claim that retail flow is an important determinant of market direction. If that’s true, it’s a huge problem.I agree-the reason is me I have written About Recent-The flow is generally very important. However, we are not yet convinced that retail flows (rather than institutional flows and buybacks) dominate.

However, what is very interesting in the JPM report is the idea that retail equity flows may also support the fixed income market.

Aggressive purchases of stocks and equity funds by certain retail investors, perhaps younger cohorts, can significantly boost the stock market, causing “other” retail investors, or older cohorts, to inadvertently overvalue stocks. Will be. To prevent the equity weighting from rising excessively, these “other” retail investors are buying fixed income funds for rebalancing. .. .. So it’s no coincidence that the strong equity returns of the last few years, such as 2019 and 2017, were also the years of very strong fixed income fund flows. .. .. The background to this rebalancing is that future stock market adjustments could lead to a sharp decline in rebalancing flows in the fixed income market as well.

Below is a JPM chart of Global NetFlow to Equity and Fixed Income Mutual Fund ETFs.

It’s very important if recent equity and fixed income rallies are linked by portfolio rebalancing. The negative correlation between equities and bonds is very important to investors as it is the most important hedge in most portfolios. It is very bad for stocks and bonds to lose support at the same time.

But there are two questions. For example, why did strong net equity flows in 2013 and July 2006 not drive strong bond flows in those years? Did the discussion not apply at that time? And if old cohort investors are rebalancing into bonds, shouldn’t they sell stocks to do that to offset the influx of young cohort investors?

Details of tricky topics in retail flow over the next few days.

Nearly final comment on private equity returns

Tired of reading about Private Equity Fund returns? Perhaps, but people aren’t tired of sending me emails about them. The debate, “Does PE outperform the public market?” Makes unhedged readers bubbly.

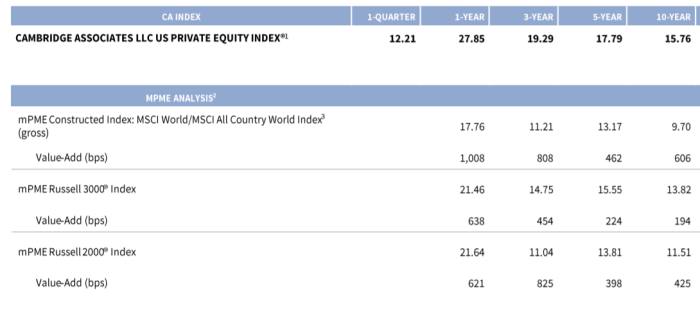

I asked the reader to send proof of outperformance for the last 10 years. One reader submitted the Cambridge Associates US Private Equity Index figures. With an annual rate of return of almost 16% over the last decade, it is about 2% higher than the Russell 3000. This is a huge deal.

It happened that a prominent private-equity skeptic warned that fund consultants and PE managers would all quote Russell’s small cap index. The S & P 600 has a 10-year annual rate of return of 15.4%, just 30 basis points below the Cambridge Index.

Now all together: PE industry! It wasn’t significantly above the public market! The last 10 years!

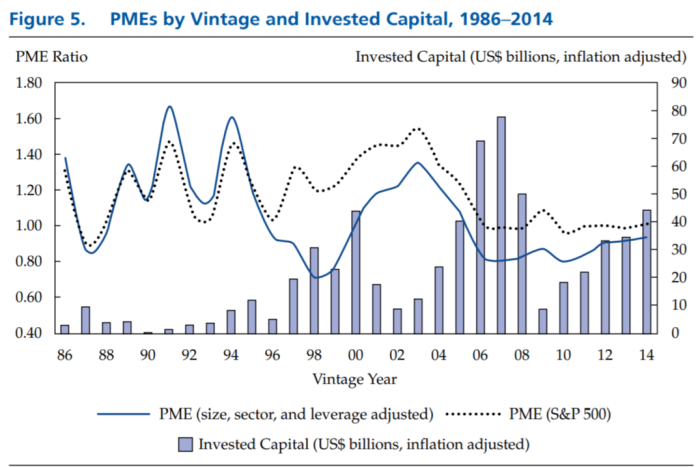

Sent by another reader this A well-designed study of PE returns from 2016 (“Bottom-up approach to risk-adjusted performance of the buyout fund market”). The author, a major pension system analyst, worked really hard to get the right comparison. They use data on 752 buyout funds formed between 1986 and 2008. This includes specific information about the dates of cash inflows and outflows into the fund through 2015.

They use this data to build a public market equivalent (PME) ratio, which is a measure of “how many dollars you need to invest.” [public markets] Benchmark per dollar for buyout funds. ” They then adjust public benchmarks to match the size, sector composition, and leverage of the company in the buyout fund. The most important thing is to value-weight PE returns. So a fund that worked very well (for example) but didn’t attract a lot of capital didn’t distort the results.

Conclusion? “We found no evidence of outperformance from the US buyout fund market.” That is, the PME ratio was not significantly different from 1. If the authors are right, PE has been profitable like a public market for over a decade on a risk- and value-adjusted basis. Below is the key chart. A PME of less than 1 indicates poor performance compared to public benchmarks.

{kind=link}

Interestingly, however, the author argues that PE investment adds value.

We believe that buyout funds play a valuable role in the portfolio of institutional investors. First, they offer small cap exposure and expand the set of opportunities available to public equity investors. This is an important portfolio addition, especially when the small cap stock market is thin, such as outside the United States. Second, the ability to choose a good manager is valuable. Due to the large cross-sectional diversification of buyout fund returns compared to public equities, buyout funds offer a more attractive opportunity to exercise managers’ choices.

The latter point chimes in many of the emails I receive. The important thing many readers argue was to invest in the best PE managers. The best PE managers can be identified in advance, as they will continue to perform above average from one fund to the next. I will address this important argument (and the other one or two bits of PE folklore) soon.

One good reading

China perhaps Communist country.

Recommended newsletter for you

due diligence — The world’s top story of corporate finance.sign up here

Swamp memo — Expert insight into the crossroads of money and power in US politics.sign up here

Hot retail summer | Financial Times Source link Hot retail summer | Financial Times