{kind=link}

There have been few happier investors than Intel (INTC 2.47%) and AMD (AMD +2.13%) investors in 2026. If you purchased shares at the start of 2026, the returns have been phenomenal. Intel’s stock essentially tripled, while AMD’s stock is up around 140%. Those are fantastic results, but both stocks have shown weakness in the past few days.

Since the calendar flipped to July, there has been heavy selling pressure on these two names, and AMD stock has plunged more than 10% while Intel is down 20%. That’s a major sell-off in a short time frame, but does that mean it’s time for investors to panic and sell the stock? Or is this a prime buying opportunity? Let’s find out.

Image source: Getty Images.

The turnaround is still ongoing for these two

AMD and Intel have a theme in common: They’re both turnaround plays. Both AMD and Intel have lost to their chief rivals in recent years, and the market is betting on a major turnaround.

AMD is trying to gain ground on Nvidia (NVDA +3.90%) in the GPU marketplace. The biggest growth area for this product line is in the data center space, where Nvidia has outright dominated AMD. However, there were hopes that AMD could gain some ground back on Nvidia.

During the first quarter, AMD’s data center division grew 57% year over year to $5.8 billion in revenue. That’s a notable improvement over previous quarters and a strong result overall, but it’s just not Nvidia. During Nvidia’s Q1, its data center division generated $75.2 billion in revenue, rising 92% year over year. So not only is Nvidia nearly 15 times larger, but it’s also growing far faster.

Today’s Change

(2.13%) $11.62

Current Price

$558.34

Key Data Points

Market Cap

Day’s Range

$540.26 – $560.19

52wk Range

$141.90 – $584.73

Volume

547.1K

Avg Vol

36.5M

Gross Margin

47.09%

It doesn’t look like AMD is doing anything special versus the undisputed industry leader, Nvidia, so I have doubts about AMD’s strength.

Meanwhile, Intel is chasing competitors on two fronts. For its chip division, it’s actually competing against AMD. However, the bigger focus for Intel has been its chip foundry business, which competes against Taiwan Semiconductor Manufacturing (TSM 0.55%) During Q1, Intel’s foundry division grew revenue by 16% to $5.4 billion. Once again, it was outperformed by TSMC, which saw revenue of $35.9 billion, rising 41% year over year.

Today’s Change

(-2.47%) $-2.78

Current Price

$109.76

Key Data Points

Market Cap

Day’s Range

$107.46 – $110.85

52wk Range

$18.96 – $142.35

Volume

3.5M

Avg Vol

134.3M

Gross Margin

35.90%

The market expects Intel and AMD to be incredible turnaround plays, but the reality is that the companies that have been dominating them in recent years are still far superior. To make matters worse, each is expensively valued.

Expectations priced into the stocks are too high

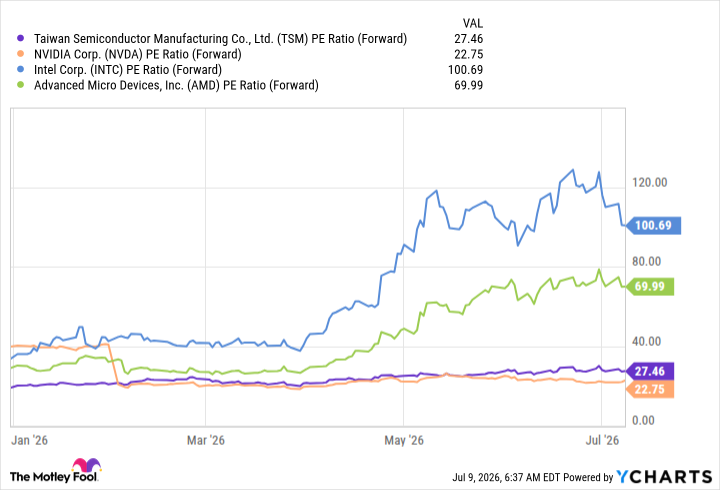

Looking at the valuations of Intel and AMD also reveals another key factor: All of the turnaround that really hasn’t occurred yet has already been priced into the stocks. AMD trades for 70 times forward earnings, while its rival Nvidia trades for 22.8. The same goes for Intel, which trades for 100 times forward earnings compared to TSMC’s 27.5.

TSM PE Ratio (Forward) data by YCharts

For these two to grow into their valuations and trade at similar levels to their rivals, Intel must increase its earnings fourfold beyond 2026’s projections. AMD is a little less aggressive, but it still must triple its earnings beyond 2026’s predictions. That’s a monster performance, and with its rivals continuing to grow their earnings and revenue at a remarkable pace, the bar will keep moving higher for the companies to reach a reasonable valuation.

As a result, I think selling Intel and AMD in favor of their rivals makes the most sense. These two stocks have run up a ton and likely have gotten far too ahead of themselves. Meanwhile, TSMC and Nvidia trade at attractive valuations, and I think investors will be far more satisfied with the long-term returns of these two than with AMD and Intel.