{kind=link}

The tech sector now makes up 35% of the S&P 500. And a big reason for that concentration is the growing number of tech stocks with massive market caps.

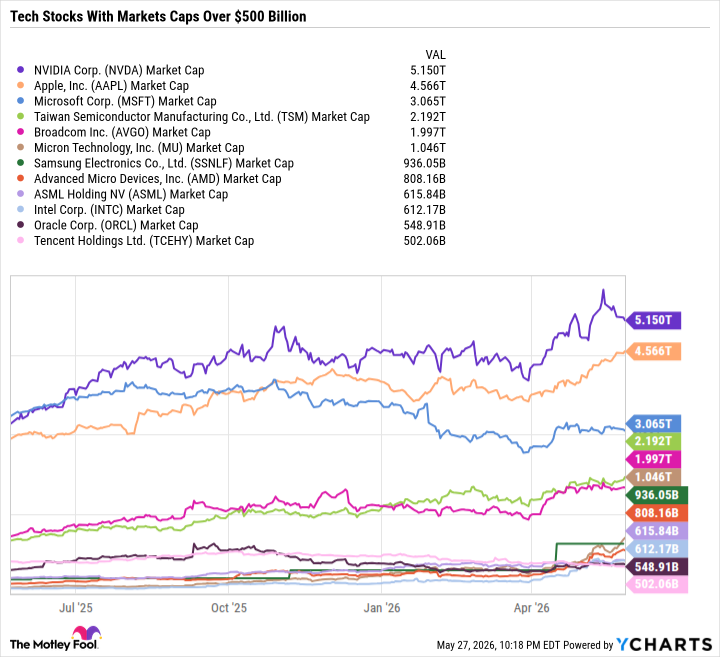

There are 11 companies with market caps over $1 trillion, and five of them are U.S. tech stocks. Micron Technology officially joined the $1 trillion club on May 26, while Eli Lilly, Walmart, and Samsung Electronics have all been in the club but are just below the threshold at the time of this writing.

With a market cap of $808 billion, Advanced Micro Devices will probably be the next tech stock to join the $1 trillion club. Behind AMD is ASML (ASML +0.46%) at $616 billion and Intel at $612 billion.

Here’s why ASML has the clearest path toward becoming the next tech stock to join the $1 trillion club and why it’s a great buy now.

Image source: Getty Images.

ASML is ahead of the AI curve

ASML has quietly become Europe’s most valuable company and is now worth more than double the market cap of second-place LVMH. ASML is also the most valuable semiconductor equipment company in the world, ahead of Lam Research, with a $399 billion market cap; Applied Materials, at $356 billion; and KLA, at $256 billion.

Data by YCharts.

ASML has a virtual monopoly on extreme ultraviolet (EUV) lithography machines, whereas Lam Research and Applied Materials compete in deposition, etching, and polishing equipment, and KLA dominates the process control market.

Many modern chip manufacturing processes use low numerical aperture (Low-NA) EUV machines, but next-generation chips for artificial intelligence (AI) workloads will rely on ASML High-NA EUV machines. The technology is so new, not to mention incredibly expensive, that ASML is only selling one or two High-NA machines per quarter.

High-NA is just getting started, but low-NA EUV is in full swing, as ASML’s EUV sales (High-NA plus Low-NA) are now roughly double non-EUV sales. However, more than half of ASML’s revenue still comes from general-purpose, less advanced deep ultraviolet sales plus services on its installed base of existing equipment in the field.

Today’s Change

(0.46%) $7.40

Current Price

$1613.17

Key Data Points

Market Cap

$622B

Day’s Range

$1604.92 – $1653.84

52wk Range

$683.48 – $1654.20

Volume

50.8K

Avg Vol

1.7M

Gross Margin

52.60%

Dividend Yield

0.54%

Going beyond the data center

ASML is a catch-all way to invest in AI rather than choosing between custom chip and AI networking companies such as Nvidia or Broadcom, memory giants such as Micron versus Samsung Electronics, or cloud computing titans such as Amazon, Microsoft, or Alphabet.

Data center server racks contain graphics processing units (GPUs), central processing units (CPUs), memory chips such as high-bandwidth memory (HBM) and dynamic random access memory (DRAM), and associated networking and interconnects. So one rack could theoretically contain Nvidia GPUs, AMD CPUs, Micron HBMs, and Cisco Systems networking and interconnects. Chip giants such as Nvidia and Broadcom are pushing to take rack-scale market share by designing custom AI chips and providing AI networking. But the point remains that there’s a lot of competition for space on hyperscale data center server racks.

Rather than competing for market share within the data center, ASML exists further up the value chain at the manufacturing level. It doesn’t mind if Broadcom takes market share from Nvidia or Micron gains on Samsung Electronics. And it’s indifferent if a company is fabless, like Nvidia, AMD, and Qualcomm; designs and manufactures some of its own chips, like Intel and Samsung; or manufacturers the vast majority of its chips, like Micron and Texas Instruments. Rather, ASML wins so long as the broader industry continues to grow in size and sophistication, boosting demand for the commercial-scale precision manufacturing lithography equipment that only ASML can provide.

ASML breaks down its net system sales, which excludes servicing its installed base, by logic (processing) and memory (data storage). In the first quarter of 2026, logic made up 49% of net system sales, and memory was 51%. In the same quarter from 2025, logic was 58% and memory was 42%. Despite the shift from logic to memory, ASML’s sales grew 10.5% year over year — showcasing how the company benefits from AI-driven demand regardless of the ebbs and flows in logic and memory.

Looking ahead, ASML is also well positioned to benefit from the AI inferencing boom. ASML also stands to gain from growth in physical AI, such as robotics and self-driving cars, as those end markets would require advanced chips manufactured with ASML’s machines.

An AI stock built for multidecade growth

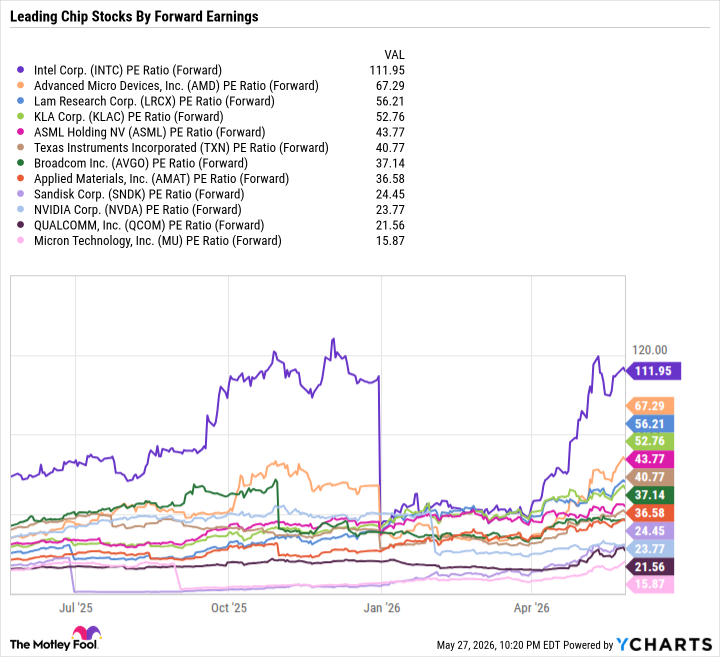

The biggest risk to ASML is that AI doesn’t produce the return on investment that companies hope for, which leads to lower capital investment and, in turn, less need to expand chip manufacturing capacity. Another risk is that new competition emerges to challenge its market share and, in turn, its profit margins. And finally, that ASML’s future returns will be underwhelming, given it already trades at a premium of 43.8 times forward earnings.

Data by YCharts.

However, no company has come close to replicating ASML’s High-NA EUV technology. And ASML’s high cash flow enables it to invest heavily in research and development to maintain its competitive advantage.

ASML is no stranger to enduring the semiconductor industry’s cyclical slowdowns. It has the business model and balance sheet to ride them out and capitalize on the cycle when it shifts — exiting first quarter 2026 with 7.97 billion euros in cash and cash equivalents, compared with just 2.71 billion euros in long-term debt.

ASML will be a clear winner from continued advancements in generative, agentic, and physical AI. If ASML continues to generate double-digit earnings growth, it’s only a matter of time before it joins the $1 trillion club.

Daniel Foelber has positions in ASML, LVMH Moët Hennessy-Louis Vuitton, Nvidia, and Oracle and has the following options: short July 2026 $200 calls on Oracle and short October 2026 $220 calls on Oracle. The Motley Fool has positions in and recommends ASML, Advanced Micro Devices, Alphabet, Amazon, Apple, Applied Materials, Broadcom, Cisco Systems, Eli Lilly, Intel, Lam Research, Micron Technology, Microsoft, Nvidia, Oracle, Qualcomm, Taiwan Semiconductor Manufacturing, Tencent, Texas Instruments, and Walmart. The Motley Fool recommends Lvmh Moët Hennessy-Louis Vuitton, Société Européenne. The Motley Fool has a disclosure policy.