{kind=link}

Shares of Palantir Technologies (PLTR 2.16%) have slipped 30% in 2026, as of this writing, primarily due to the stock’s expensive valuation.

Investors have chosen to overlook the fantastic growth in Palantir’s revenue and earnings, which continue to improve with each passing quarter. However, opportunistic investors may now be wondering if it would be a good idea to buy Palantir stock following its pullback. That’s why we will take a closer look at Palantir’s valuation and prospects in this article to decide if it is worth buying right now.

Image source: The Motley Fool.

Palantir Technologies remains expensive, but that’s half the picture

Palantir has a trailing earnings multiple of 134. The forward earnings multiple of 81 points toward a big jump in its bottom line, but it is still on the expensive side. The tech-focused Nasdaq Composite index, for comparison, has an average earnings multiple of 41. Even the sales multiple of 59 represents a significant premium to the index’s average price-to-sales ratio of 5.5.

Today’s Change

(-2.16%) $-2.58

Current Price

$116.92

Key Data Points

Market Cap

$280B

Day’s Range

$116.18 – $120.91

52wk Range

$116.18 – $207.52

Volume

1.2M

Avg Vol

44.4M

Gross Margin

84.07%

However, it won’t be correct to look at Palantir’s valuation in isolation. The company’s growth rate makes it clear why it trades at a premium. Palantir’s revenue in the first quarter of 2026 rose 85% year over year to $1.63 billion. The company reported a 154% jump in non-GAAP earnings per share to $0.33 per share.

For comparison, the technology sector’s earnings in Q1 were anticipated to increase by 45%. Palantir’s growth was significantly better, justifying the premium it trades at. More importantly, the company’s earnings growth rate has been improving due to higher spending by existing customers and the addition of new customers.

This has helped Palantir build a healthy revenue pipeline, which is likely to ensure solid growth for years to come. Specifically, Palantir signed $2.4 billion in new contracts in Q1, significantly exceeding its top line. As a result, the company’s remaining deal value (RDV), which refers to the total value of contracts yet to be fulfilled at the end of a quarter, nearly doubled year over year to $11.8 billion.

The size of Palantir’s RDV suggests that its growth rate could improve once it starts converting its significant backlog into revenue. Moreover, the fact that Palantir received more business than it fulfilled in Q1 is evidence that demand for its AI software platforms remains robust.

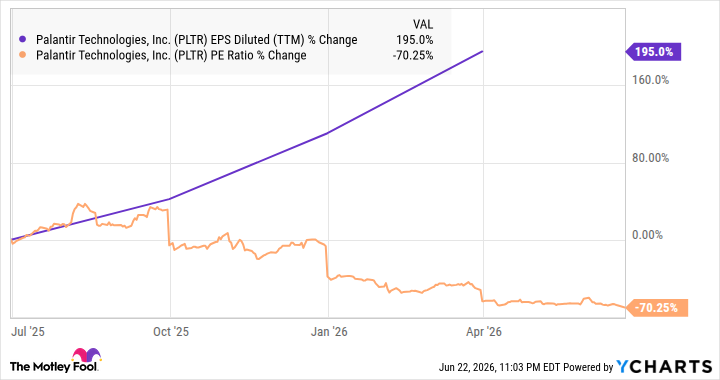

The market isn’t giving Palantir enough credit for its solid growth and prospects

Palantir’s earnings have jumped impressively over the past year, but its price-to-earnings ratio has dropped significantly.

Data by YCharts

This suggests that the market isn’t rewarding Palantir’s solid growth and prospects, creating an opportunity for growth-oriented investors to buy the stock. Moreover, Palantir operates in a market whose size is on track to grow exponentially. According to one estimate, the global AI software platforms market could grow from $31 billion this year to a whopping $237 billion in 2034, as enterprises and governments integrate this technology into their operations to boost productivity.

Palantir’s 2026 revenue guidance of $7.66 billion suggests that it is a major player in this emerging space. That’s why investors with a long-term investment horizon can consider utilizing Palantir’s pullback to buy this AI stock, as it can come out of its rut and deliver healthy gains on the back of the secular growth opportunity in AI software.