{kind=link}

DenisTangneyJr/E+ via Getty Images")

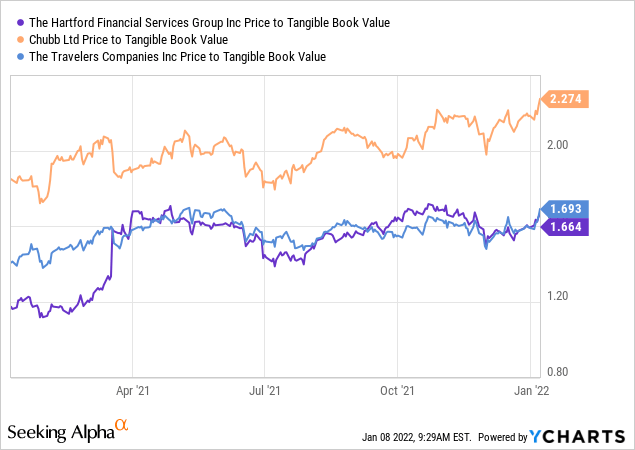

Hartford Financial Services (NYSE:HIG), a diversified financial company offering commercial insurance, personal insurance, group benefits, and mutual funds across the US, recently held its virtual investor day featuring optimistic commentary on the health and prospects of the business over the medium to longer-term. In particular, the P&C (“property & casualty”) insurance underlying combined ratio and ROE guidance were bright spots, reflecting expectations for recent favorable trends to continue into the upcoming years. Yet, HIG trades below P&C peers as investors continue to view it as a ‘show me’ story, likely only providing credit for results when delivered. But over time, I think the relatively low P/B value compared to its strong ROE and book value growth should result in a re-rating.

Compelling Setup for Commercial Heading into 2022

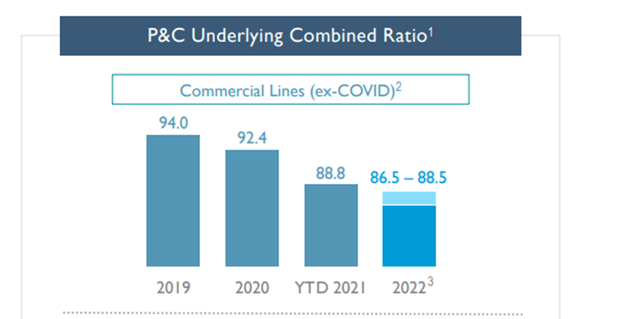

HIG reaffirmed the near-term guidance laid out with its prior earnings report, with commercial lines NWP (“net written premiums”) growth guided at 4% to 5% in fiscal 2022 with an underlying combined ratio of 86.5% to 88.5% (vs. 88.8% YTD). While the flat guidance might disappoint some investors, management did indicate it is running ahead of plan with commercial lines growth coming in at 11% this year and expected to hit 4.5% in fiscal 2022, implying a solid 7-7.5% CAGR. And while HIG refrained from updating its margin guidance (beyond the 2%pts of underlying improvement expected in 2022), management commentary signaled pricing would not fall below loss in the near term.

Source: Hartford Financial Services Presentation Slides

Interestingly, the event also offered a rare glimpse underneath the hood at HIG’s commercial business, providing important insight into enhancements the company has made in recent years. Most impressive was the profitability of the new Spectrum policy, which has produced an 85% underlying combined ratio in fiscal 2021. While the benefit from light non-cat property losses in FQ3 ’21 likely boosted the ratio somewhat, the fact that HIG’s new business line is already enhancing margins is a key positive. With the Navigators acquisition outperforming targets as well, HIG looks set to further build out its growth capabilities in specialty going forward.

Positive ROE Guidance Outweighs Investor Day Disappointments

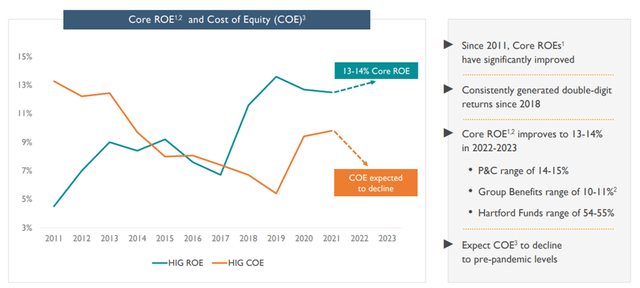

Hartford has also guided to a core ROE of 13% to 14% in fiscal 2022 (modestly above the 12.6% averaged over the 2018-2020 period), comprising P&C (14% to 15%), Group Benefits (10% to 11%) and Hartford Funds (54% to 55%). The underlying ROE could prove even stronger, however, considering the Group ROE is lower than P&C, which management attributed to a higher mix of intangibles in the segment. As such, on a tangible basis, Group would have contributed (not proven dilutive) to the overall ROE. I view the updated targets as achievable in light of the strong momentum on the core P&C side and the potential for share repurchases ahead. While there may have been some disappointment that HIG did not discuss plans to look for alternatives for the Mutual Funds business, I think the key positives from the event more than outweighed the modest disappointment here and of not raising targets. Instead, I think many of the offsetting factors for HIG remain unappreciated, including its extensive new products across almost all businesses and its improving expense levels.

Source: Hartford Financial Services Presentation Slides

Favorable Capital Allocation Update

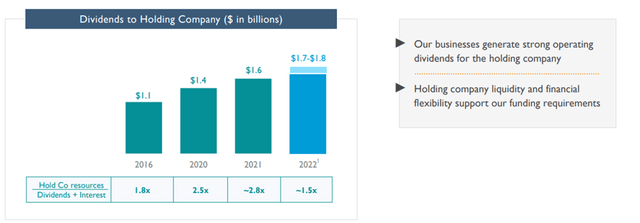

Perhaps the most salient update from the investor day presentation was that HIG now has all the products it needs to achieve profitable growth and market-leading ROEs. This means plenty of excess capital will be available for use for both shareholder return (dividends and repurchases) and future growth ahead, although M&A remains a low priority. On the dividend front, HIG is guiding toward hold co dividends of $1.7-1.8 billion in fiscal 2022 (up from the $1.6 billion guided for fiscal 2021), with much of the increase coming from its P&C subsidiaries. Furthermore, HIG is also projecting a similar level of repurchases in fiscal 2023 relative to the annual pace in fiscal 2021/2022, implying another $1.5 billion based on the YTD run rate. I see further upside to the repurchase run-rate, however, if HIG normalizes its remittance capacity from current low levels – for context, the P&C division remits 75% of statutory earnings compared to 90% by its peers. With plenty of capacity at the holdco as well, considering HIG prefunded $600 million in debt, the balance sheet flexibility could also support an accelerated capital return ahead.

Source: Hartford Financial Services Presentation Slides

Final Take

The key takeaway from its recent investor day was the fact that Hartford’s ongoing transformation into a leading P&C, group, and mutual fund complex appears to be running ahead of schedule. Yet, investors still do not appear to be giving HIG much credit for the solid underwriting and growth initiatives or the recent operational improvements, with its three key businesses all poised for margin expansion ahead. In the meantime, shares appear substantially undervalued – HIG trades below P&C peers Chubb (NYSE:CB) and Travelers (NYSE:TRV) despite being on track for a strong 13-14% ROE. Over time, ROE and book value growth should drive the valuation, leaving plenty of scope for outperformance ahead.