{kind=link}

jetcityimage/iStock Editorial via Getty Images

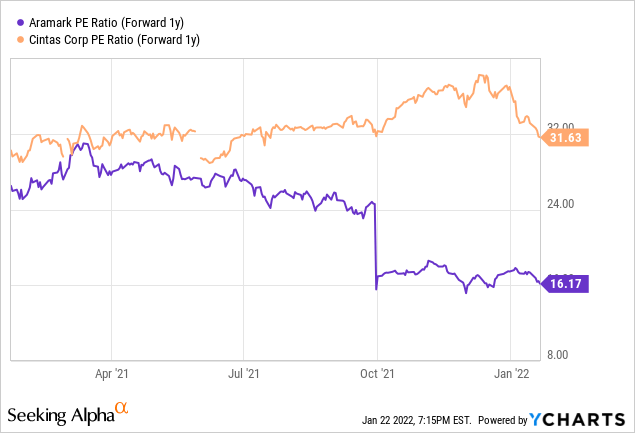

The key takeaway from leading food, facilities, and uniform services provider Aramark’s (ARMK) latest investor day event was the unveiling of its ambitious new fiscal 2025 targets, suggesting a significant growth and margin acceleration (relative to historical numbers) ahead. Recent changes in leadership, organizational focus, and culture should also help ARMK extend its recent momentum on net new business growth into the upcoming years, boosting the achievability of its longer-term growth targets. Assuming ARMK shares hold the current c. 16x P/E valuation multiple, then the midpoint of guidance (discounted back at the cost of equity) would equate to considerable upside from current levels, keeping me bullish.

Laying the Foundation for a Post-COVID-19 Growth Paradigm

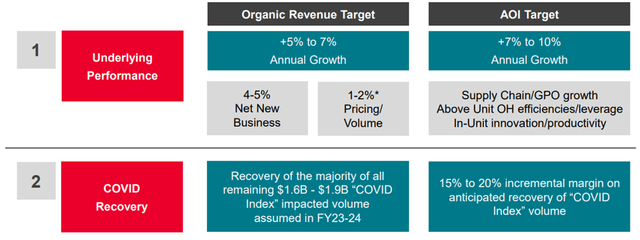

Encouragingly, ARMK’s messaging at the event was focused primarily on accelerating top-line growth, having rebuilt its leadership in each segment of the organization. As part of this focus, the updated fiscal 2025 targets are as follows – $20+ billion in revenue (comprising 4-5% net new business growth, 1-2% price/volume growth of the existing business, and the recovery of COVID-19 revenue), along with $1.6-$1.9 billion in adj operating income (implying a solid 7-7.5% margin range vs. fiscal 2022 guidance of 5-5.5%). While the targets seem ambitious at first glance, I also see some conservatism here as the pricing/volume component assumes inflation returns to normalized levels over time – if inflation were instead to remain at current levels, there would therefore be upside to these numbers as prices get passed through. There could also be upside from the remaining $1.6-1.9 billion in the recovery of COVID-19 impacted volumes, with the majority only guided to be realized in fiscal 2023/2024. And considering hybrid work trends are only set to impact white-collar employees (equivalent to 4-5% of the overall business), I see limited ongoing impact from any shift to hybrid work within the B&I segment going forward.

Aramark Investor Day Presentation

Newly Installed Uniform Division Head Impresses but No Spinoff Yet

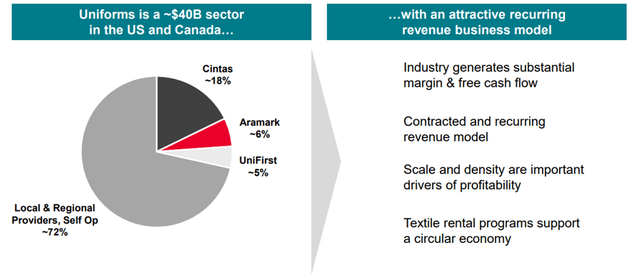

If the investor day presentation was anything to go by, the hire of former COO of TMX, Kim Scott, as President and CEO of the Uniform business, appears to be a smart move. Notably, she emphasized the roll-out of ABS (“Automated Billing System”), which is now 70+% complete, to move the Aramark field team towards client service and cross-selling. The segment is also looking to ramp up newly hired headcount, continuing the hiring spree during the pandemic (+35% increase in salesforce personnel) to get to full productivity. Beyond that, key levers to improve performance within the Uniform business include improving route density and merchandise management, both of which remain issues for the segment. With the Uniforms addressable market opportunity also pegged at a massive $40 billion, with plenty of incremental share capture opportunity available considering c. 72% of that is owned by smaller providers, the organic growth runway is extensive.

Aramark Investor Day Presentation

Also worth noting is management reiterating the Board’s openness to considering how to maximize value via potential strategic alternatives for the Uniform business. In the near term, however, the strategy remains to improve the business internally before initiating any potential transaction. I view this as a prudent step – considering peers Cintas (CTAS) and UniFirst (UNF) trade at a wide EV/EBITDA range in-line with their organic growth and margins, improving the fundamentals should precede any spinoff process for the Uniform business. As Aramark Uniform is currently posting slower organic revenue growth and lower margins than Cintas, I agree that the optimal path to maximizing value likely lies in providing the new CEO with the necessary resources to implement a full-scale transformation.

Balance Sheet Flexibility Underpins Capital Allocation Priorities

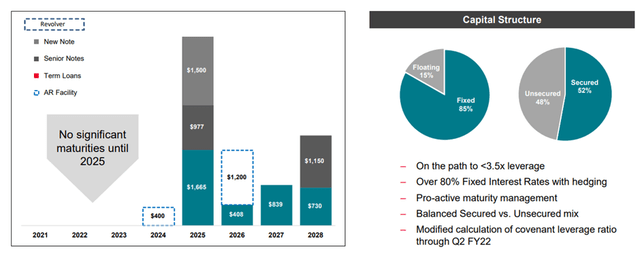

ARMK’s capital allocation priorities remain unchanged – the focus is on organic growth investments followed by opportunistic tuck-ins, along with debt paydown and quarterly dividends. As the company de-levers, however, management expressed its openness to other potential cash return opportunities – note that the current net leverage target is for 3.0-3.5x by fiscal 2025, well below the 8.2x at end-2021. I view the target as well within reach, considering the company has no debt maturities until 2025 while also benefiting from flexible debt covenants and an attractive fixed/floating rate balance. Also worth noting are the several tranches of callable notes in 2022, including the $1.5 billion 6.375% COVID-19 Notes due 2025, all of which present compelling near-term deleveraging opportunities.

Aramark Investor Day Presentation

Looking ahead, ARMK has also guided toward $2.5 billion in FCF generation over the next four years, targeting 50-55% FCF conversion rates as a % of adjusted operating income –considerably higher than the historical c. 45% level despite cash flow seasonality set for a return in the upcoming fiscal year. Coupled with the flexibility of the ARMK business model, a return to a predictable cash flow stream in a normalized, post-COVID-19 environment leaves the company well-positioned to manage its leverage profile heading into fiscal 2022. The balance sheet position also opens up M&A optionality, allowing ARMK to remain opportunistic, particularly in the international business, as it looks to expand its services across key regions.

Final Take

Overall, this was a positive investor event from Aramark, with management’s confident tone in hitting its medium-term 5-7% organic growth target on the back of consistent net new business wins, likely to underpin margin expansion as well through fiscal 2025. With fiscal 2021 results signaling that recent management changes and strategic initiatives are already yielding results, I view management’s targets as reflecting an upside scenario supporting the positive risk-reward ratio. Additional upside optionality could also come from potential strategic alternatives for the Uniform segment, as the newly installed president and CEO of Aramark Uniform Services drives a full-scale transformation in anticipation of a spinoff down the line. Relative to the current discounted 16x P/E, ARMK shares offer compelling value.