{kind=link}

Duolingo (DUOL 0.50%) operates the world’s largest digital language-education platform. I’ve followed the company for several years, but its stock was consistently more expensive than the broader market, so I waited on the sidelines for an opportunity to buy. Last month, that chance finally arrived.

Duolingo has lost 83% of its peak value over the past year. Investors are worried that artificial intelligence (AI) will disrupt its business. But they’re also concerned about management’s plan to target faster user growth, which is expected to be a headwind for the platform’s revenue and profits in the short term.

As I’ll explain, I think those concerns are overblown. And since Duolingo stock has never been this cheap (as measured by two widely used valuation metrics), I decided this is a no-brainer buying opportunity.

Image source: Getty Images.

AI is actually benefiting Duolingo’s business

Duolingo makes money in two ways. It shows advertisements to its free users, and it also offers paid subscription options for users who want to unlock additional features to accelerate their learning. The platform ended 2025 with 52.7 million daily active users (DAUs), for growth of 30% year over year. A record 12.2 million users were paid subscribers, a number that was up 28%.

AI has become a big part of the company’s strategy. Users who pay for either Super Duolingo or Duolingo Max subscriptions are granted exclusive access to a feature called Video Call, which allows them to practice their foreign-language speaking skills with an AI-powered digital avatar named Lily. She adapts to each user’s fluency level and offers supportive guidance, but in keeping with Duolingo’s fun and lighthearted approach to education, she does so with a sarcastic and playful tone.

Users who opt for the more expensive Duolingo Max subscription can also access other AI-powered features like Roleplay, which guides them to improve their foreign-language conversational skills through a chatbot-style interface.

Investors might be concerned about users potentially abandoning Duolingo in favor of AI-powered chatbots and other new tools. However, based on the strong growth in the platform’s user base, its gamified approach to education is clearly resonating. And based on subscriber growth, AI appears to be a valuable asset, not a threat.

Today’s Change

(-0.50%) $-0.45

Current Price

$90.08

Key Data Points

Market Cap

$4.2B

Day’s Range

$89.36 – $94.18

52wk Range

$87.89 – $544.93

Volume

84K

Avg Vol

2.7M

Gross Margin

71.68%

Faster user growth could pay off significantly in the long run

Duolingo generated a record $1.04 billion in total revenue during 2025, for 39% growth from the previous year. The company also delivered a record $414.1 million in generally accepted accounting principles (GAAP) net income, soaring by a whopping 367% year over year.

Those glowing growth rates might be under threat with the recent shift in Duolingo’s business strategy, so I can sympathize with investors who are concerned. Management believes investing more aggressively in acquiring new users will lead to much better financial results over the long term, so monetization is going to take a back seat for now.

Simply put, having more users will give the platform more prospects to convert into paying subscribers. Plus, in an increasingly competitive and AI-driven landscape, having a larger user base will make Duolingo much harder to disrupt.

Management will aim to have 100 million daily active users on the platform by 2028, which would be nearly double the 52.7 million it served at the end of 2025. In my opinion, Duolingo will be generating much higher revenue and earnings two years from now if that goal is achieved.

Duolingo stock has never been this cheap

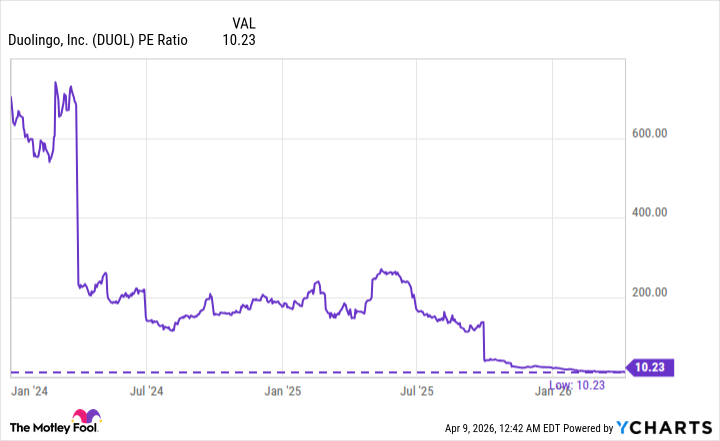

Based on Duolingo’s 2025 earnings of $8.31 per share, its stock is trading at a price-to-earnings (P/E) ratio of just 10.2. This is the cheapest it has ever been since the company went public in 2021; it’s also a 56% discount to the S&P 500 (^GSPC 0.11%) index, which trades at a P/E of 23.5. In other words, Duolingo stock looks like a bargain following its 83% decline.

DUOL PE Ratio data by YCharts.

There is a catch. Wall Street expects Duolingo’s annual earnings to decline to $7.07 per share during 2026 (according to Yahoo! Finance) because of management’s focus on user growth. However, that means its shares are still trading at an attractive forward P/E ratio of just 12.9.

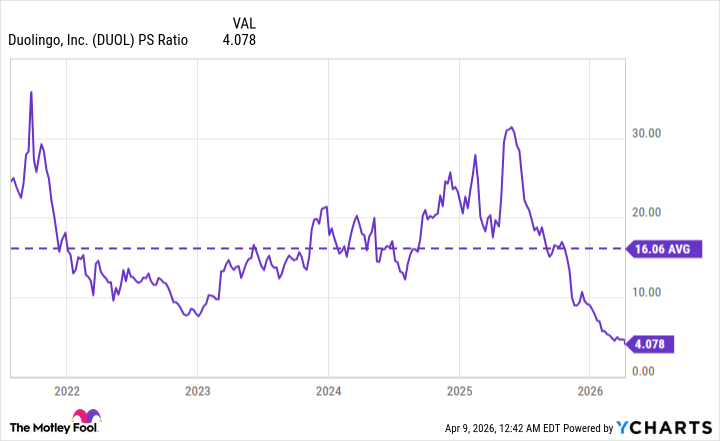

Moreover, based on Duolingo’s 2025 revenue of $1.04 billion, the stock trades at a price-to-sales (P/S) ratio of just 4.1, which is also its cheapest level since going public. Plus, that’s a 74% discount to its long-term average of 16.1.

DUOL PS Ratio data by YCharts.

In summary, Duolingo stock looks very attractive no matter which way you slice it, which is why I decided to buy. I think investors who are willing to hold onto their shares until 2028 (and beyond) are likely to do extremely well.