{kind=link}

AMD has been a solid stock over the past few years. Since the start of 2025, it’s up by more than 120%. However, I think AMD shareholders should enjoy their moment in the sun now, because there could be some cloudy days ahead.

Currently, the stock looks to be trading on the hopes that the company will gain market share from Nvidia (NVDA +1.23%), but I think there are some other companies it needs to watch out for, too. I have three stocks that I think have far more upside than AMD and will crush its performance over the long term.

Image source: Getty Images.

AMD’s growth is nothing compared to these three

First, we need to cover what’s going on with AMD. Since the start of the construction boom in data centers for artificial intelligence (AI), it has consistently played second fiddle to Nvidia in graphics processing units (GPUs).

Investors hoped that AMD could gain ground, but that hasn’t occurred yet. During the fourth quarter, AMD’s data center division experienced 39% year-over-year growth. While that’s a decent figure, it’s nothing compared to others I would rather own.

Today’s Change

(6.69%) $19.03

Current Price

$303.52

Key Data Points

Market Cap

$464B

Day’s Range

$286.17 – $304.10

52wk Range

$90.12 – $304.10

Volume

1.9M

Avg Vol

37M

Gross Margin

45.99%

Nvidia is the obvious choice since it’s competing in basically the same field. During its fourth quarter, its data center division produced 75% year-over-year growth.

Another emerging competitor in the AI chip space is Broadcom (AVGO +5.06%). The company isn’t designing general-purpose GPUs like Nvidia or AMD. Instead, it’s partnering directly with AI hyperscalers to design custom chips that are narrowly suited for the specific workloads they are expected to see during their useful lives.

This is a rapidly growing business segment: Broadcom’s AI semiconductor division grew its revenue 106% during its latest reported quarter. In 2027, management expects this division alone to generate over $100 billion in revenue. For reference, AMD’s data center division brought in $5.4 billion during the fourth quarter.

Another less obvious competitor for AMD is Amazon (AMZN +2.18%). It’s most famous for its e-commerce site and delivery services, but it also has a booming cloud computing division. And its custom-designed AI chips are quickly growing in popularity.

The annual run rate for the company’s chip business recently exceeded $20 billion, and that segment is growing at a triple-digit percentage pace. It has several new rounds of chips coming, and their planned manufacturing runs are already nearly sold out.

As a result of all of this competition, AMD could struggle to grow meaningfully in the data center space, which would be a major problem for its stock.

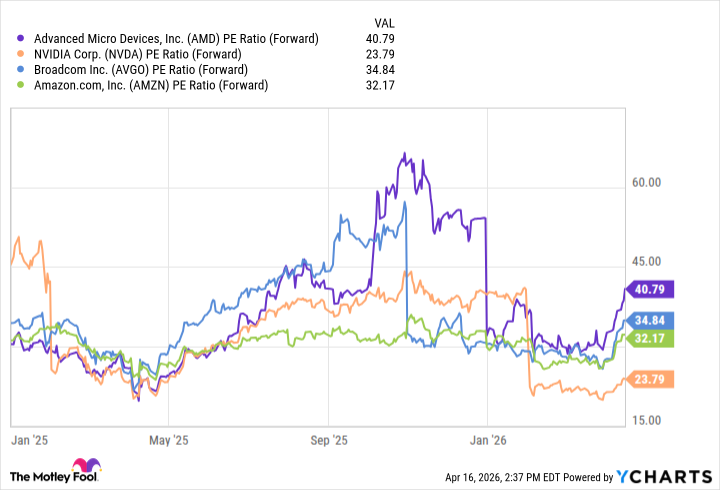

AMD has a premium valuation

Despite AMD not having growth as good as this trio, its stock trades at a premium.

AMD PE Ratio (Forward) data by YCharts; PE = price-to-earnings ratio.

It’s not often that the worst-performing stock of a peer group (in terms of growth) trades at the highest premium, but that’s exactly where AMD is.

That doesn’t bode well for AMD, especially if these other three can keep up their impressive growth. As a result, I’m more bullish on Nvidia, Broadcom, and Amazon.

With the AI data center construction boom expected to last through at least 2030, there is plenty of upside for everyone involved in this trend, including AMD. However, its share price already has a ton of anticipated growth baked into it, making me less bullish about its upside potential.

Nvidia, Broadcom, and Amazon are in the right place at the right time to take advantage of the massive spending going on. AMD is a bit late to the party and may not be able to dig itself out of its hole. Its GPUs are often viewed as a second-choice option relative to Nvidia’s chips, and with other viable options beyond GPUs emerging from Broadcom and Amazon, their shares are more logical picks than AMD.