{kind=link}

If you had invested $20,000 in Vertex Pharmaceuticals (VRTX 1.26%) in its IPO in 1991 and held onto its shares, you’d have over $1 million today, considering the company’s strong 14% compound annual growth rate since then, much better than the S&P 500‘s 11% over the same period. Maintaining this pace over more than three decades is commendable. However, can Vertex Pharmaceuticals still perform well from here on out?

Image source: The Motley Fool.

The past few years haven’t been great

Vertex Pharmaceuticals has made quite a name for itself, given the company’s dominance in its core market. It develops medicines for a rare disease called cystic fibrosis (CF), characterized by the accumulation of thick, sticky mucus in the lungs, which leads to a range of problems, including respiratory issues. Vertex Pharmaceuticals is the only notable player in this niche. Its portfolio of CF medicines has improved over time, enabling it to treat about 95% of CF patients in the U.S.

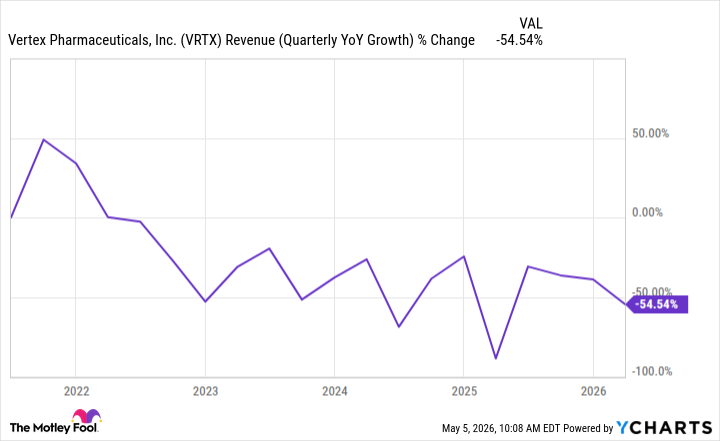

However, as the biotech leader has made progress in this field, its top-line growth rates have declined. In the first quarter, Vertex’s revenue increased by 8% year over year to $2.99 billion. That’s not terrible, but Vertex Pharmaceuticals has seen a general downward trend on this front in recent years.

VRTX Revenue (Quarterly YoY Growth) data by YCharts

What’s more, although the drugmaker is trying to diversify its lineup and reduce its exposure to its core therapeutic area, its efforts in that regard have thus far been somewhat unsuccessful. That’s why Vertex Pharmaceuticals has lagged broader equities over the past three years.

Reasons to be optimistic

Despite its struggles in non-CF markets, things may be about to pick up for Vertex Pharmaceuticals. The company expects at least $500 million in non-CF revenue this year. That’s significant for Vertex Pharmaceuticals, since in 2024 it reported $10 million in revenue from products outside CF, which grew to $175.4 million last year.

Today’s Change

(-1.26%) $-5.42

Current Price

$424.43

Key Data Points

Market Cap

$108B

Day’s Range

$412.52 – $432.70

52wk Range

$362.50 – $507.92

Volume

103K

Avg Vol

1.4M

Gross Margin

87.68%

Things will likely improve further in 2027. Vertex Pharmaceuticals is now seeking approval for Casgevy, a gene editing medicine for sickle cell disease (SCD) and transfusion-dependent beta-thalassemia (TDT), for patients between the ages of five and 11; Vertex Pharmaceuticals co-markets Casgevy with CRISPR Therapeutics. The median age of death for SCD and TDT patients is 45 and 37, respectively, hence the importance of treating them as early as possible. That’s why this label expansion is important for Vertex Pharmaceuticals.

Meanwhile, the company is racing toward approval of povetacicept, a therapy for IgA nephropathy (IgAN), a kidney disease. Povetacicept could become a major growth driver, especially if it earns indications beyond IgAN. Even in CF, Vertex Pharmaceuticals will likely seek to develop new products, as it has in the past, including some to treat the remaining 5% of patients it can’t reach with its current medicines. My view is that, within a few years, Vertex Pharmaceuticals will have a much deeper, more diversified portfolio, helping it post stronger revenue and earnings growth.

And the company’s core CF business that can still perform relatively well, along with a deep pipeline, makes its long-term prospects bright. For all those reasons, Vertex Pharmaceuticals looks attractive at current levels.